One of the more interesting angles of the China financing story is the way it is hampering Venezuela’s ability to weather the current slump in the oil prices.

Here is the lowdown on the renegotiation with China:

“The MOFCOM article goes on to explain that the declining oil price requires Venezuela to export more oil, but that Venezuela is unable to increase production in the short-term. The Venezuelan government therefore sought to extend the loan period.”

This was mirrored in a recent Wall Street Journal article, which said,

“… Venezuela ships oil to Cuba and other Caribbean countries through special agreements, and doesn’t earn cash on it. It also ships hundreds of thousands of barrels to China annually, to pay off tens of billions in loans made by Beijing, say former oil industry executives … Now, with the price of oil falling, Venezuela will have to pony up even more barrels to China to cover its debts. Meanwhile, up to 800,000 barrels a day are consumed domestically at pennies on the gallon.”

The China loan deals Venezuela has embarked on the last few years are making a bad situation considerably worse. Here is why.

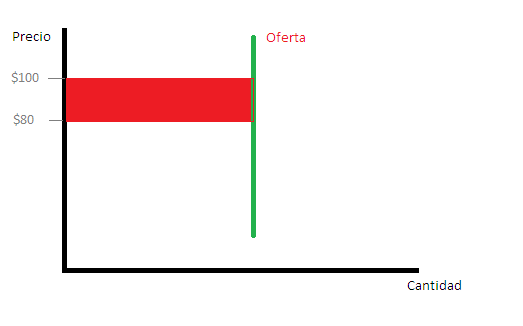

Imagine, if you will a country that always sells a fixed amount of oil, no matter the price. You could say that country has a vertical supply curve – irrespective of what the price is, the quantities sold do not change much. Many industries exhibit vertical supply curves – for example, chances are that your local movie theater will offer the same amount of seats regardless of the price of movie tickets.

Since income is given by price (P) times quantity (q), we can say that for countries with vertical supply curves, a drop in the price of oil means lost income equal to the difference in price times the amount you sell. In this graph, the lost income would be given by the size of the read, very red area – the area of the rectangle is the price differential times the quantity.

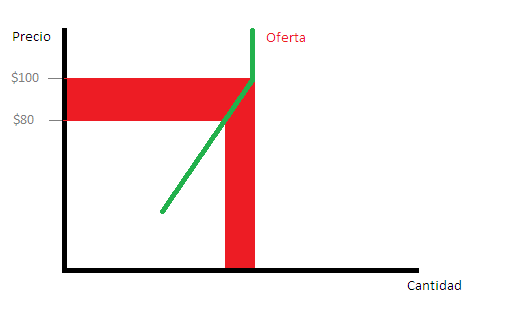

Venezuela, though, does not have a vertical supply curve. That is because the China loan agreements stipulate that when the price of oil falls, Venezuela must ship more oil to China to compensate, leaving fewer barrels available to sell to international markets. In other words, Venezuela has a positively sloped supply curve – a fall in prices is accompanied by a fall in the quantities available to markets.

In other words, the graph for Venezuela doesn’t look like the one above, but rather like the one below.

Notice how much larger the red, very red area is.

The situation is quite simple. Because of the loans we signed with China – them paying in advance for future shipments in oil – the drop in oil prices means Venezuela doesn’t just sell each barrel for less money, it also has fewer barrels available to sell to the market. Venezuela’s downturn is therefore made all the worse by the ridiculous conditions the geniuses at PDVSA signed on to.

In other words, a bad situation is made worse, and the hit in our fiscal income is all the larger.

And why was all of this done? Why were the agreements with China signed in the first place?

Cue Chávez’s economic guru, a certain Mr. Giordani:

“In this stage of the Bolivarian process, it was crucial to overcome the elections of October 7th, 2012, as well as the elections of December 16th of that year. Consolidating political power was an essential objective for the strength of the revolution y for the opening of a new stage in the process. Overcoming these obstacles required a great sacrifice met with an economic and financial effort that brought the use of resources to extreme levels, something that had to be reviewed in order to guarantee the sustainability of the economic and social transformation.”

Thanks, very good explanation of the situation. Two points. One, I recommend reading the Chinese government statements directly. Google translate works wonders. Second, to answer your final question, don’t forget that Chávez was a true believer in peak oil. They probably thought that the opposite situation would prevail, that they would be able to pay the debt with much less oil than predicted. A country already overwhelmingly long oil took out margin to go even longer on the same commodity. The current pain in Venezuela is the classic result of inadequate portfolio diversification.

LikeLike

Excellent analogy! Thanks Setty.

LikeLike

To be a believer in Peak Oil doesn’t mean you believe prices will rise dramatically into the stratosphere.

For Chávez and others on that side of the Ocean it did, evidently. Fracking is just one of the responses to that.

LikeLike

Spot on! So along the same lines one could make the case that Margin Calls will start to trigger soon (if not already).. I expect a lot of noise in the Venny bond market if oil breaks the 80$ per barrel mark.

LikeLike

Is this the first time we are learning about the actual terms of the China loans?

LikeLike

Juan: Last weeks decree (October 10th.) changes the rules, such that Venezuela no longer has to send a minimum amount of barrels per day, but an amount established by “diplomatic channels”. Its a strange solution, China recognizes they can’t pay, but keeps the three year period for payment.

LikeLike

Yes, it’s some sort of default. Funny that we seem to have defaulted on China before Wall Street. Still, the terms they signed onto are ludicruous – who thought that raising the oil shipped to China when prices dropped (a pro-cyclical policy if I’ve ever seen one) was a good idea?

LikeLike

Well, as I understood from the change in the terms, the three year period was also dropped, hence the ‘diplomatic’ arrangement from now onward. The question remains on what are the hidden conditions of the restructuring.

LikeLike

Nope, the three year period was not dropped.

Gaceta is here: http://www.tsj.gov.ve/gaceta/octubre/10102014/10102014-4100.pdf#page=2

If you look at the new article 1 (which replaces Art. 3), tranches A and B continue to be paid in three years, only C seems to not have the three year period. Some people think this was an error of omission.

LikeLike

See your Gaceta, raise you a Chinese state press release: http://www.mofcom.gov.cn/article/i/jyjl/l/201410/20141000760994.shtml

“The amendment also abolished the term loan to pay off China three years”

LikeLike

My Chinese is rusty, but you are right. Then, how do we interpret it? Tranche C is now open , the other two (closer to being paid) still have three years.? Is so easy to follow this stuff…

LikeLike

The terms make sense if you look at it in terms of money though. If a barrel was worth $100 and your payments were $100 a month you could send a barrel every month and be fine, but if the price of oil falls and your payments don’t you’d still have to give your creditor $100 every month, so you either give them a barrel and the difference in tender or you give them more barrels.

LikeLike

That is right. The original terms were just like any other loan where you pay in cash. It does not matter if the crude is sold to the chinese or to any other buyer. The amount of dollars received by Venezuela (and subsequently paid to China) is exactly the same.

The graphic is misleading because the extra red column on the right side is still received by Venezuela, the fact that is earmarked to pay the chinese debt makes no difference.

What the new agreement does is flexibilize the payment terms allowing for payments that are lower in $ than what the loan originally required.

The original FT article says that PDVSA could sell as many barrels to China for payment as they want, which seems extremely flexible. But the Gaceta article instead remarks that the minimum crude amounts should be agreed upon by both parties via diplomatic notes and that Venezuela must sell at least that amount. Venezuela still should sell above the agreed minimum in order to satisfy the loan terms AS LONG AS NOTHING IMPEDES IT (that is the flexible part). That does not make it look as flexible as the FT article says.

LikeLike

Sure, but it’s highly pro-cyclical. Furthermore, you *could* have made the loan contingent on the price of oil by including a clause that said that Venezuelan payments each year are a function of its oil income or something like that. That way you isolate public finances a bit more when the going gets tough.

LikeLike

I’m not tracking, Juan. Why would China (or any creditor) want to do that? Unless you get an equity upside (or believe that it reduces default risk) there’s no reason to sign that sort of contract. What am I missing?

LikeLike

Maduro’s latest statements on these financial shenanigans go something like this:

“We will no longer turn to the international capital markets for financing [since they rejected us – by default (ironically, hehe), since they demanded extravagant terms].

But luckily we have some friends who are willing to help us out [wink, wink…] !!”

The equivalent of getting rejected at the bank and turning to a loan shark. Let’s hope the chinese play nice.

LikeLike

Maduro’s best credit default swap and protection may come, o irony, from el imperio norteamericano.

Sure, China is a loan shark. But it’s a loan shark that cannot deliver on the skarking part of the business.

Nothing in Venezuela will budge the US into any form of action. Nothing, except overt foreign intervention from outside the Western Hemisphere. If China tries anything substantial to recoup its rotten loans, Uncle Sam will come knocking, and knocking hard. The Chinese know that. Heck, even Maburro may know that.

So, yeah, why not default on the Chinese? What’s the point of keeping them current if no more money is forthcoming from them (as they signaled)? They can’t do a thing to get their

moneybarrels back.LikeLike

Another great piece by Juan !!, Of course the financing is not paid in oil bls , its paid by the proceeds from the bls sold to China which are deducted from the amounts actually receieved by Pdvsa so that if the price falls then the quantity of shipments has to rise so as to make up for the lost revenues. The new arrangement doesnt have to reduce the volume of bls sold to China only the propportion of the price which is deducted to pay for the financing per each sold shipment , implying an extention to the payment period.

Not sure about the math , 350.000 bls per day is equal to aprox 360 million of bls in 3 year which at 95-100$ per bl equals some 35 billion $ of financing which Ramirez announced some months ago Venezuela had received from China (plus a 4-5 billion additional financing which Venezuela was then negotiating,), Interest is about 6% (half the financial market rate of Venezuelan bonds) .

By extending the payment period on the Chinese financing on a negotiated basis, the fall in prices doesnt have to prevent the regime from continuing to pay its international bondholders .

Once again what Venezuela faces is a fall in revenue which in part is due to falling oil prices but which is worsened by the fall in its capacity to produce light medium crudes and instead having to produce a bigger propportion of extra heavy crudes which profitability is much lower because of the need to mingle it with imported light medium crudes and refined diluents and the more costly logistics of doing so.

LikeLike

Some Chavista with brain will read this and scratch his head wondering himself if someone is misleading him, i hope

LikeLike

Actually Juan, I do not understand the fuss with the chinese loans. Had venezuela borrow the money instead from the voluntary capital markets would not have to sell more oil to continuing serving that debt? There is nothing special on the chinese loan conditions that make it particularly procyclical. In fact, de facto (even if not de jure) the chinese loans are proving to be actually more flexible, aparently allowing the Venezuelan government to pay less (dollars, reminbis) at a time when oil prices are going down. If anything I register this as a plus for the chinese deal. If Venezuela is refinicing its debt with China instead of with Wall Street, it might be because it is easier and less costly/painful.

We might critizice the chinease loans on many accounts (transparency for example), but on prociclycality? Not at all! If anything, it is the other way around.

LikeLike

Well, I guess if all loans are pro-cyclical, the Chinese ones are pro-cyclical as well. In other words, we are getting just a regular loan, as any other, but without the transparency, and with enormous corruption.

When the general public thinks about the loans to Chine (it they think about it at all), they believe it’s something like a fixed number of barrels per month. “Loans for oil” and all that … you lend me some money, and I promise to send you 350,000 barrels per day. If the price of oil drops, well tough, you’re taking on the risk. As it happens, it’s the Venezuelan people who are assuming the risk of the global oil markets – a dip in the price of oil means China gets more oil, and Venezuela sells less oil to international market.

LikeLike

Yes, but that is not the idea the reader gets from your post

LikeLike

There is no difference between selling oil to China or to the international market.

LikeLike

Yes, the ups and downs. When oil went up Venezuela would need less oil to repay the loan. So it could be sais that China “took the risk” in terms of oil barrels.

I am sorry Juan, but you are being bias on this one, you just dont want to accept it.

LikeLike

The Chinese loans are cheaper too!

LikeLike

Well, another little fact that keeps proving that chavismo deliberately ruined Venezuela, destroying its economy and its population’s chances to progress.

And all of it because the wax doll.

LikeLike

The elephant in the room no one sees is why did Venezuela borrow from China in the first place?

Can the loans from China be traced to see where the money went? If it went into Hugo Chavez’ personal bank account then Chavez’ estate should give it to the government to pay back China. If the borrowed funds went to Cuba, then Cuba should pay it back to China.

LikeLike

The main problem is that the proceeds of the loan were used in… something that does not, and will never produce additional revenue to pay itself. So the trick is not the form in which you pay the loan but what you do with the new money in the first place.

Lets say that Chavistas enjoyed (or mismanaged or simply stole) the proceeds of the loans and we are the ones that are paying the bill, because lets face it, the infrastructure that produces the oil used to pay was in place before they arrived, all they did was to mortgage the house that they inherited and party the mortgage moneys for 15 years, hasta que el cuerpo aguante.

LikeLike

mortage-for-party-funds analogy is very powerful.

The parents have just returned from their holidays, to find the mess from the house party …

The other powerful reality here is that the nation, and the opposition parties in particular have been utterly negligent in safeguarding the nation interests. Perhaps (surely!) some where invitees to the orgy…

LikeLike

In Chavez’s own words, his primary mission was to make the revolution “irreversible”, i.e. wipe out private enterprise. Trashing the economy was the method used.

LikeLike

The USA is often condemned for either lack of altruism or lack of sufficient altruism. No one will ever be able to accuse the Chinese of altruism in their dealings. The Chinese do self-interest, and do it very well.

LikeLike

Quick question here. The second graph seems to suggest that, the higher the price, the higher the quantity produced. I might be wrong, but that contradicts what is written just before.

Shouldn’t supply curve be vertical when the price equals 100, and then downward sloping and to the right as soon as the price starts to fall?

LikeLike

Never mind, I got it. The graph is showing the loss Venezuela incurs by diverting barrels from the international market and selling them to China. Now, my question is, why does it matters who is Venezuela selling the barrels to? Aren’t all buyers tied to the same price?

LikeLike

I’m surprised that nobody mentions the reduced demand from USA!

LikeLike

The reason why Pdvsa bought US refinery marketing systems abroad was precisely so that if prices went down no one else could ( by lowering their price ) drive venezuelan oil supplies from that market. Pdvsa by securing a marketing outlet for its crudes always keep its share of that market even if net revenues from that market fell a bit.

LikeLike