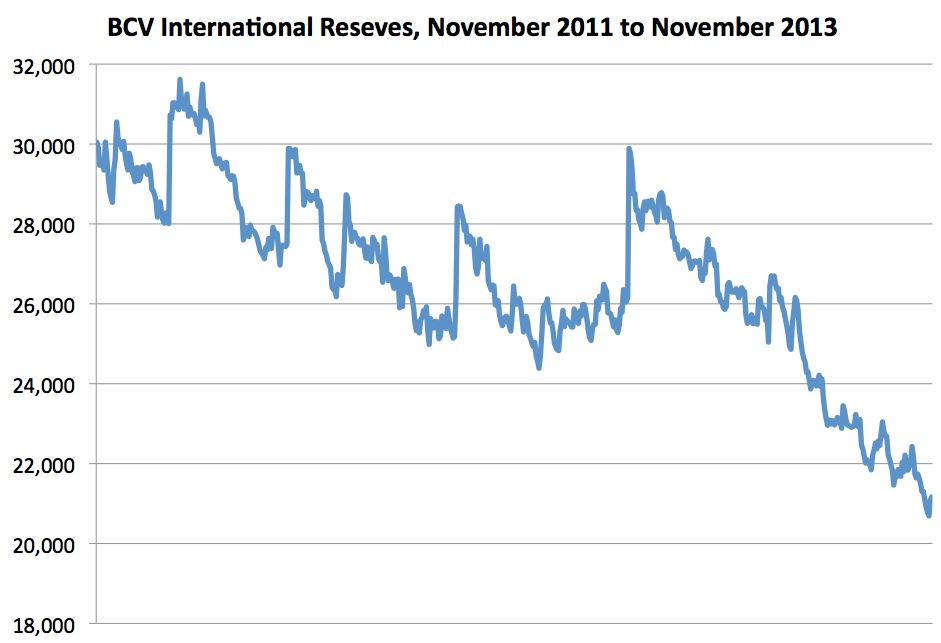

One way to make Omar Lugo’s dismissal matter is to really stop to understand the front-page spread that got him canned. The story that the regime found so objectionable is that the Central Bank’s international reserves are falling at unprecedented pace. They’re half what they were at the start of 2009 and have been falling at a staggering billion dollars per month recently.

One way to make Omar Lugo’s dismissal matter is to really stop to understand the front-page spread that got him canned. The story that the regime found so objectionable is that the Central Bank’s international reserves are falling at unprecedented pace. They’re half what they were at the start of 2009 and have been falling at a staggering billion dollars per month recently.

Remarkably, the liquid portion of reserves is pretty much gone, leaving the government with the humiliating prospect of having to cash out the gold reserves that Hugo Chávez brought into the country to such fanfare two years ago.

But how can that be? So far, the Maduro administration has been just one big paquetazo, as measure after painful measure is taken to stanch the flow of hard currency. We already had a 32% nominal devaluation, CADIVI’s increasingly a black hole that no dollar escapes from and SITME/SICAD has been shut down for much of the year.

After all we’ve been through, after all the bare shelfs and the shoving matches for perniles and the scary inflation spike this year and the harsh cuts on public spending, you’d think we’d at least come out the other end having stabilized our Central Bank reserves, wouldn’t you? That’s what Bank of America’s FRod seems to think: that Maduro’s paquete has brought Venezuela’s foreign accounts to some sort of rough balance.

And yet, despite all the pain, BCV still finds itself with reserves a third lower than they were at the start of the year, and falling faster all the time. How can that be?

Over on Distortioland, Omar Z. starts to sketch out an answer. It gets pretty technical pretty fast, but the nub of it is that external balance isn’t just about the external accounts: a domestic monetary imbalance can drive a fast drawdown in BCV’s foreign reserves, even in the middle of an external adjustment.

To grasp why, you have to think like a macroeconomist – an exercise most of us muggles find tantamount to cruel and unusual punishment, to be sure, but one that will become increasingly unavoidable in the months and years to come, so best get used to it.

Let’s give it a go:

Last week, as we looked at the pictures of long lines outside Daka, most of us saw people trying to get something: a nice new TV, say, or an Air Conditioner. But macroeconomists saw something else. They saw people desperate to get rid of something, namely: the fast-depreciating bolivars in their pockets.

It wasn’t just a case of mindless consumerism, of mere rapiña. People were making a rational decision to trade something whose value they’re sure will fall – bolivars – for something whose value seems more likely to hold steady – appliances.

The length of those lines is a testament to the increasingly widespread belief that tomorrow’s bolivar is going to be worth a lot less than today’s. If that’s what you believe, your best bet is clear: spend your bolivars as soon as you get them. After all, you’re better off holding almost anything bolivars can buy rather than holding those fast self-destructing bolivars themselves.

When that way of thinking starts to spreads, the economy shifts onto a highly perilous new path.

The operative bit of jargon here is the “demand for money” – people’s willingness to hold bolivars rather than the things bolivars can buy, whether that’s a plasma screen TV, a pair of fake boobs or a DPN bond.

Omar Z. argues that, for most of last few years, the demand for bolivars has been propped up by the control raj: price controls, capital controls and, especially, exchange controls have conspired to pen in demand for bolivars by cutting people off from many of the alternatives to holding them (chief among those alternatives: the US dollar).

That’s one of those things that works for a while, and then stops working. As the government covers more and more of its deficit through BCV’s printing press, as inflation rises and the expectation starts to take hold that it will keep on rising indefinitely, and as confidence that the BCV has some idea what it’s doing evaporates, the control raj finds it increasingly difficult to sustain the demand for real bolivar balances.

But what does any of that have to do with those fast falling BCV reserves? That’s where Omar Z’s post proves so valuable. It brings much needed clarity to the question of why, when the supply of money (a.k.a., liquidity) is rising at the same time as the demand for money is falling, that will turn up in the national accounts in the form of depleting Central Bank reserves.

If you’re mathematically minded you absolutely should go to his blog and see for yourself why that must be so. But you don’t have to get into the equations to grasp that if people are increasingly eager to trade their money for real assets, and a big portion of those real assets are imports paid for in dollars, BCV reserves will come under pressure (since, ultimately, BCV reserves is where the dollars that pay for the imports must come from.)

There’s no easy way out of this mess. In principle, BCV could take even harsher measures to stop the net outflow of reserve assets, or even stop them altogether…but that would defeat the purpose, shifting the burden of adjustment onto even harsher shortages and even faster inflation, as more and more bolivars chase a fewer and fewer imported goods. Insisting on one-in-one-out conditions for reserve dollars would simply recreate today, when there are still $21 billion in the till, the conditions that would prevail if reserves ran out altogether. And that would be a good way of triggering the hyperinflationary spiral they’re supposed to be trying to prevent.

So BCV reserves are going to continue to fall. Because liquidity keeps expanding and, in Omar Z’s view, leading indicators suggest that the demand for real money balances is already starting to falter.

Now, if you’re at all sensitive to economic history, talk of faltering demand for real money balances amid rising liquidity will be setting off all kinds of alarm bells in your head: that way hyperinflation lies.

To be sure, we’re not there yet: a hyperinflationary freakout would probably come after reserves run out altogether, and even though they’re depleting way too fast, $21 billion is still a good chunk of change. (And, lest we forget, even after that’s all gone, there’s an unknown extra cushion in the off-budget funds such as Fonden.) So, to be clear, an apocalyptic crash doesn’t appear to be imminent.

The direction of travel is clear, though. Worse: there’s no sign that the people in charge have even begun to grasp the need for a change of course. If you’re accelerating towards an abyss in a car with no brakes and a driver hell-bent on ploughing straight ahead, it’s not much comfort to be told “relax, we’re not in any imminent danger: that abyss is miles away.”

What’s more, in this context, “imminent” is a slippery term. Because, as Omar Z. explains in a passage that manages to be chilling even through a thick haze of jargon:

Entre otros factores, sabemos que la demanda de dinero también depende de las expectativas de inflación, que a su vez puede ser una función de factores como la velocidad de expansión monetaria y la credibilidad del BC (¡!). Es decir, la solución de esta simple ecuación pudiera ser recursiva y bajo ciertas condiciones ser dinámicamente inestable.

In other words, the fact that it’s taken 11 months for BCV reserves to fall from $30 bn to $21 bn in no way guarantees that it will take another 11 months to shave off the next 9 billion dollars.

The demand for money could turn out to be like boots and hearts: when it starts to fall apart, it really falls apart.

Silly question: what would happen if after the elections Maduro were to devalue the currency once more and, because there are no immediate elections, spend less on Chinese Haier or cars? It would be just like before another patch, another temporary solution, inflation would again hike, the government will have many more Bolívares to spend. Would reserves – ceteris paribus – be depleted at a slightly slower pace then, at least for a few months?

I think lots of economists and development specialists around the world wonder what’s our secret as Venezuelans to fail where other succeed.

Oil dependency, Dutch disease square and all that: yeah, but it still doesn’t explain it. Our nation has a special knack for screwing itself up.

LikeLike

Another elections are 15 months ahead, and much more important that time around (legislative). He most certainly will go down the road you describe, but certainly not enough to actually fix the imbalances, for electoral reasons.

What you say at the end is terriby true. Venezuela has a special knack to screw itself up :/

LikeLike

But perhaps it’s like: 10 months of slowing down and then 5 months of madness…if

we don’t get into politcial whirlpool, that is.

Can some economy illuminatus tell us what would happen to the reserves if we had a one time devaluation of, say, 40%, 50% right after the elections, all other things being equal?

LikeLike

I second the question, would such a move stabilize the reserves?

A highly related question – how big devaluation would be necessary to stop the drain?

We’ll see how much of a risk Maduro is willing to take in about a month or so. He will most likely devalue again around Christmas break.

LikeLike

One thing you can be assured of, Maduro will start the campaign for the next election on 9 December.

LikeLike

Nope. Maduro will create a law making him the only legal candidate. Just like Cuba.

LikeLike

Thats easy: nothing. Official E/R and Black E/R are pretty much independent. That is, unless you have access to official dollars. Therefore, it is irrelevant at what E/R the government devaluates a market that you don’t have access to, in the same way a price increase in Ferraris would affect the prices on Toyotas. The black market exists because the official market is not able to cope with the demand for dollars. And the demand for dollars is that high because the incentives of the economic agents to convert their bolivars into dollars are still there (demand for bolivars falling, expected inflation, Black E/R, you name it), until the Gov or BCV change their strategy, which no one expects in the near future.

That being said, unless the official rate matches the black rate, at which point the black market would disappear, the reserves will continue to drop, and the black market rate will continue to rise. But that is not prone to happening because the arbitrage resulting between these two markets is one of the ways the Gov has to distribute PDVSA rent, maintain clientelism and support (keep the armed forces happy and wealthy) to keep the piñata going.

LikeLike

For the Nth time we’re off chasing the shiny thing – a discussion on the forex market – and missing the real underlying problems: deepening debt monetization, out of control money creation and a BCV that is run by a donkey.

FORGET ABOUT THE FOREX MARKET. It’s a red herring.

There is no Forex policy that is consistent with macroeconomic stability when you have deepening debt monetization, out of control money creation and a BCV that is run by a donkey.

(And any Forex Policy is consistent with macroeconomic stability as long as you stop monetizing the debt, bring money creation under control and get someone minimally competent to run BCV.)

LikeLike

I agree with you that the main issue in your article is the macroeconomic stability, but it is bold to say that the forex market is irrelevant, since it is one of the main decision-driving factors that affect the economic agents under the actual circumstances. You cannot achieve stability in one instance and just leave the other distorted, because they are connected and one affects the other. In fact, this is the main point of Omar’s article on distortionland: how a macroeconomic unbalance is having effects in the country’s foreign accounts.

LikeLike

Of course. I’m overstating out of frustration. CADIVI is maybe 20% of the problem, but it’s 99% of the discussion!

People seem to think there is some magical formula through which a reform of forex policy could enderezar el entuerto. It just ain’t so.

LikeLike

The bottom line, besides all the economic jargon is that you can keep up and extremely unproductive economy, heavily controlled by the state, sustained by a crazy monetary policy in a country that imports everything. But the thing is that the crazy monetary policy is a huge part of the reason that you have been able to hold power for 14 years so it would be political suicide to do it.Under than scenario, just eliminating CADIVI could make matters worst.

LikeLike

There’s a lot of confusion about this. What the economy needs is a *real* bolivar depreciaton, not a *nominal* devaluation. If you devalue 50%, but inflation keeps running at 50% per year, then you end up exactly where you started. You’re just spinning your wheels.

To get a real depreciation, you’d need to simultaneously devalue and take drastic steps to bring down liquidity. Omar doubts that this is even possible in current circumstances. It would be politically very, very tough. It may not be possible at all.

LikeLike

I understand (or think I am understand) a devaluation now would simply be a temporal patch, to reduce a little bit of pressure for a little time – just like the government has so badly done over the years.

Some – I think Miguel Octavio also – think the best would be to do away with the currency control once and for all, which would mean a dramatic devaluation and huge inflation for a couple of months and then stabilization -. Chavismo will never do that, obviously.

The option in the second paragraph is to devalue to some level (which implies keeping crawling peg system) AND to radically cut off government expenses?

LikeLike

Reinier Schliesser, commenting on Omar’s blog, explains what’s so dangerous about this kind of approach:

La otra cosa importante acerca de la demanda de dinero es que su relación con las expectativas de inflación (valor de la moneda) es no lineal. Eso quiere decir que podemos estar lentamente transitando esa trayectoria hasta que un buen día un shock cualquiera eleva las espectativas por encima de un umbral que hace caer estrepitosamente la demanda de dinero. Por eso es que las inflaciones altas son intrínsecamente inestables. Un dia tienes inflación alta y al siguiente..bum! hiperinflación…

Yo creo que estamos peligrosamente cerca de ese riesgo. Eso no quiere decir que estemos cerca de una hiperinflación, pero estamos caminando tan cerca del precipicio que cualquier brisita nos puede lanzar hacia alla.

Could a nominal devaluation meant to just relieve a bit of pressure for some time be the shock that tips you over the edge? I dunno, and I don’t want to find out…

LikeLike

A lessor devaluation would probably have a bigger impact on the black market rate. However, I think the real issue is why would anybody trade dollars for bolivars? Certainly, the exchange rate is sufficient to motivate those with dollars to buy up say real estate at bargain values. However, there is no certainty that the transaction could be deemed a “crime” and the property taken and somebody put away in prison. This is a political problem perhaps even more so than an economic one.

LikeLike

Do you like chocolate? You can go to Amazon.com and buy a 4-pack of Nestle fat-free hot cocoa mix, about 29 ounces for US$27.66.

Or you can go to Venezuela and buy $27.66 worth of bolivars, or 1,660 BsF, and then go to the gourmet shop and buy 400g bars of El Rey for 205 Bs each, meaning you can get 8 of them, or almost 113 ounces of some of the world’s best dark chocolate.

That is to say, the bolivar is currently a buy.

LikeLike

Yes. But I understand that the issue is not only the value of the bolivar. I believe that the larger point is that the policy that its the main cause of inflation and a possible BoP crisis is the excess of liquidity. But that this excess liquidity is so intrinsically tied up to the survival and viability of chavismo that it might no be possible for them to do something about it. If you just devalue without changing the monetary policy I think you might end up in a even worst place than before?

LikeLike

exact.

LikeLike

Precisely. You just can’t do something about one and let the other be. You need to work with both towards macroeconomic stabilization, otherwise it is futile. But that is not the goal for the time being because this excess of liquidity is giving the perception of well being to a broad base of voters who, -probably beginning to decline in number- still represent a vast portion of the country.

LikeLike

In fact, real devaluation implies empoverishing the population in real terms. It’s not that it’s tough, it’s that it’s impossible.

LikeLike

Thing is, if real depreciation is impossible, then hyperinflation is just a matter of time…

LikeLike

The ingredient is “hunger”, that when people are starving, they might be willing to spend everything they have on their next meal.

LikeLike

Another silly questions: The black market is illegal. Importers are being required to demontrate where they bought their dollars. Theoretically, they broke the law and the sellers of dollars broke the law. Is the government intending to eliminate the black market sell of dollars and eliminate the buyers perhaps to force the business into the government hands?

http://www.eluniversal.com/economia/131120/importers-in-venezuela-will-have-to-declare-us-dollar-origin

LikeLike

I think this is exactly their plan. To force everyone to admit they broke the law, so they can go after them for wrecking.

Their decleration of where they got the dollars from has no other explanation. Even Chavizmo can’t be THAT incompetent not to know who it sold dollars to.

LikeLike

Yes, but this is like biting the hand that feeds you! How is biting that hand going to solve anything?

LikeLike

I have been saying this over & over since they made the BM a crime.

On one hand what option do the importers have if CADIVI or SICAD will not give you sufficient $$.

In the example that I’m aware of the companies need approx. $500,000 per month to restock their stores, For the last 2+ years they have not received 10% of that through SICAD etc. & nothing from CADIVI. What option did they have? They bought on the BM, stayed open & provided employment to dozens of people.

I was talking to one of the owners yesterday & they are absolutely scared of the future. They have no idea what they will do. I would imagine they will keep on buying whatever $$ they can & try to stay in business. Maburo’s plan is to squeeze them & many others out of business. Why, other then because he can, I have no idea. The long term effects of this will be disastrous mainly to his own followers.

If they are so short of money that they are starting to sell the gold reserves they have to allow a BM or they won’t survive.

LikeLike

I just wanna say: Awesome Tragically Hip Reference!

LikeLike

I had a feeling somebody would catch that reference, but I figured it’d be canucklehead…

LikeLike

I’m probably the only guaro who has ever heard and like the Hip (unless I’m proven otherwise). Fully Completely is one of my all-time favorite albums. #CourageFTW

LikeLike

Thanks for clarifying a very challenging post by Omar, Quico. I guess the main takeaway is: if people’s expectations are such that they don’t want to hold on to bolívars, you can’t continue having CADIVI. Well, you can, but you bankrupt the country.

LikeLike

Again, a really great post! I had tried to work through Omar’s post last night, but was defeated by his ability to juggle five dependent variables, as well as the Greek letter, Sigma, in the same sentence. It appears you made it through, and came out the other side replenished and enthusiastic. Again, great job!

Anatoly Kurmanaev, Bloomberg reporter in Venezuela, tweeted on Tuesday that Maduro just told his cadena listeners to “consume less”. In other words, hold onto those Bolivares Fuertes! This is obviously more revolutionary than getting rid of your paper BFs, and could signal that someone in the regime understands the problem.

Buying stuff as a way to hold onto value could also be called “hoarding”. And will be, no doubt. Under communism, everyone can aspire to be a counter-revolutionary, even those who followed last week’s instruction to leave the shelves bare.

LikeLike

Consume less? That’s in line with the Eternal Leader’s demand for 3 minute showers.

What’s next? No chicken to buy? “Eat more slowly, chew well”

LikeLike

I forgot about the 3-minute shower limit. Add clean water to the shortage list.

LikeLike

I think that’s more in the communist mantra of consuming is bad because is imposed by the empire. Not that consuming is bad because it increases the demand for goods that must be imported and that that makes CADIVI unsustainable.

Deep down, most Venezuelans, including people in the opposition, believe that CADIVI is viable as long as it is not corrupt. They don’t understand how exchange control, per se, without the added corruption, distort the economy.

LikeLike

Special congratulations are owed Francisco for his very legible rendering of Omar Z technical explanations. Thats the kind of writing needed if we are ever to educate the mayority of Venezuelans on the complexities of modern economics . Understanding Omars explanation however is not very comforting, the govt can only hope to keep its hold on power through a total control of political and economic life and all forms of mass media . Ultimately their failure to meet the countires demand for goods and services will fray their already falling popularity.!! .

LikeLike

“govt can only hope to keep its hold on power through a total control of political and economic life and all forms of mass media.” Oh, like Cuba you mean?

LikeLike

On a less serious note: It is ironic that the FED in the USA, a bit worried about deflationary pressures, is having the opposite problem. In order to stimulate demand and crash the zero interest rate barrier they need people to think there is inflation on the horizon. Maybe they should pay the likes of Genius Giordani and Leader Maduro to consult with them and show them the way.

LikeLike

Maybe we should just swap Central Bankers. Problems fixed.

LikeLike

Janet Yellen would last how long in Carmelitas before she got secuestro-expressed? 10 minutes?

LikeLike

I know families that live in barrios in Caracas. They just told me that the government owned banks, Banco de Venezuela, Banco Bicentenario etc. recently told their clients holding credit cards that their credit is now 5x the original, and in some cases 8x the original.

At the same time Maduro is asking people to consume less?

LikeLike

Here in spanish:

http://radiomundial.com.ve/article/bancos-triplican-l%C3%ADmites-de-las-tarjetas-de-cr%C3%A9dito

“La competencia entre bancos para capturar mayor cuota de consumo plástico es voraz en estos meses. El economista y analista financiero, José Grasso Vecchio, explicó a este rotativo que “es un tema que tiene que ver con la fecha de cobro de utilidades”….Grasso Vecchio asegura que la competencia de los bancos se concentra en la cartera del consumo plástico y no en las captaciones; dado que la mayoría de los bancos tiene exceso de depósitos. Asimismo, tener mayor cuota de consumo de las TDC “ayuda a los bancos a compensar el costo de cumplir con las diferentes gavetas crediticias obligatorias”, comentó.”

LikeLike

“humiliating prospect of having to cash out the gold reserves that Hugo Chávez brought into the country to such fanfare two years ago.”

It would be more than humiliating if the gold reserves were no longer in Venezuela in government possession. Chavez always had a $hit eating grin when he publicly handled gold bars. Cuba may have increased its gold holdings over the last year.

LikeLike

Maybe this is too short run to make a difference, but the “war on speculation” may have increased the demand for money and decreased the demand for imports. That EPA communication saying they were not procuring anything else from national providers for the rest of the year, as well of the drop in the Voldemort rate would point to business not wanting to pile on inventories just so that Nickar (http://www.factmonster.com/dictionary/brewers/nickar.html) comes around to steal your stuff.

LikeLike

Again, I’m just a muggle but…is that really what a bare shelf does to the demand for money?

I guess it would increase it, since it blocks me from being able to get rid of my real money balances. But if demand for money goes into freefall, maybe that bare shelf only makes me even more frantic to find something, anything to trade my bolivars for.

So we’re back to this: “BCV could take even harsher measures to stop the net outflow of reserve assets, or even stop them altogether…but that would defeat the purpose, shifting the burden of adjustment onto even harsher shortages and even faster inflation…”

El ajuste de los anaqueles vacios…

LikeLike

Would it be patriotic to lower the prices on empty shelves?

LikeLike

I think rather that it increases the demand for currency while decreasing the demand for money (the two can be mutually exclusive) while at the same time increasing the velocity of money.

Think about that for a second.

In a normal inflationary environment, be it low levels as seen in El Imperio, or higher ones elsewhere, money and currency are synonymous with one another. However, in a true pre-hyperinflationary environment, the calling card for the transition into reallybadthings is when there is a breakdown in the relationship between money and currency. You end up with a situation similar to phonecards in Zimbabwe as a store of value and a means of exchange.

There’s been a bit of work done on this sort of scenario and the above is pretty much a hallmark of the “flip”. I think, if it isn’t quite there yet in Venezuela, it will be shortly.

I also think that, going back to reserves, everything is decided by the price of oil. They can hold out for a while and possibly scrape up some additional credit lines, but if oil should drop, the bottom will fall out pretty quickly. The depletion of reserves will continue geometrically as long as the persistent inflation continues to kick the BCV’s rear end.

Venezuela has been fortunate (or unfortunate, I suppose) that oil has been as high as it is for a relatively long time. Otherwise…

LikeLike

If you check out dollartoday they more or less are saying that the bolivar has strengthened due to colombian demand for bs (to get venezuelan gangas) and sagging venezuelan demand for dollars as stores are in no hurry to replenish stocks with st nick on the rampage…

LikeLike

With all the talk of especulacion (which i naively did not see as real speculation but increasingly i see how this is becoming a barter economy – call me slow) i was wondering what the opinion is on the role of cucuta in setting the parallel rate? How big is that market after all? Somewhat bizarre this feeling that colombians have potentially the power to dictate monetary policy, a la george soros … What would happen if venezuela demanded that colombia curb that market?

LikeLike

I think that Miguel Ángel Santos is onto something similar on this piece. http://miguelangelsantos.blogspot.com/2013/11/el-paquete-de-maduro.html

LikeLike

Sort of, but Santos follows the same mistake everyone seems to make by STARTING with a discussion of Forex controls and then following the logic back to the need to the deficit. That’s a twisted understanding of the problem, putting CADIVI first.

First you need to address the underlying drivers of disequilibrium – out of control budget deficits, fast money creation, and gimme-a-friggin’-break leadership at BCV. Do something meaningful about those three things and then come talk to me about Cadivi…

LikeLike

Giving aspirin for a headache caused by a tumor.

LikeLike

Say the opposition took over the government tomorrow. How would things get better? Is there a plan?

LikeLike

There are plans… Question is which one will win elections.

—

LikeLike

QUESTION: Limiting profits is going to be based on FIFO or LIFO accounting? This makes a HUGE difference?

LikeLike

You could put all the economists in the world end-to-end, and they still wouldn’t reach a conclusion.

LikeLike

Buuuuuu…deja la flojera y estudiate la vaina primo!

LikeLike

Te explico Primo: con lo que tu escribiste y esa frase que consegui hoy finalmente entiendo como los “economistas” chavistas (que ninguno de los que manda es economista) llegaron a las conclusiones que llegaron y se tradujeron en altos deficits, impresion de dinero, Banco central politizado y controlado, cadivi, etc.

Si los economistas nunca se ponen de acuerdo, esta cuerda de animales mucho menos, yo me imagino que giordani gano la pelea por simple insistencia y/o porque los otros que estaban discutiendo se fueron a guisar y les valio mierda lo que hiciera el loco giordani

Capiche?

LikeLike

Since the bcv is the governments de facto piggy bank, isn’t the simple explanation for the fall in reserves a contraction in the conomy and the governmnts response of spending dollars to make up for falling production (since demand has not dropped – the inflationary part since the government is also attempting to keep employment and salaries up)? Perhaps i am missing the fine print??

LikeLike

Pais de locos…hasta en Rey David están racionando la Nutela. Solo 3 potes por persona!!! Como si el gobierno estuviese diciéndoles que no pueden vender más de eso jejeje.

LikeLike

As usual, it is now time for “los toderos de turno” to bash Venezuela on debt and financing issues. Well, let’s see, I don’t really understand why people keep paying so much attention to the BCV’s economic figures and balances. Really. Do I need to remind you that Venezuela’s economic picture is very distorted and “simplistic” and “traditional” analyses don’t apply in this case? Of course we all hear about how the BCV is not working well because it was “stripped” of its independency (right, the FED, the ECB and the BOJ are so independent by the way) but then you actually take its figures very seriously when it comes to supporting your simplistic arguments.

Most of the people investing and trading Venezuelan/PDVSA bonds or really looking closely at the country’s economy know the money is not in BCV but in FONDEN and whatever other funds, so please, stop it with the whole BCV great decline alarmist cry. Really, not scaring anyone. In the meantime, Venezuela has paid back around $4bn in debt that matured this year and investors keep clip clip. Sorry prophets of apocalypse, wrong forecast, again. But keep going, we like buying cheap.

By the way, not that I really believe in everything Ramirez has to say but, isn’t the below a kind of important piece of news?

http://www.noticias24.com/venezuela/noticia/208825/maduro-y-rafael-ramirez-seran-los-anfitriones-de-la-i-reunion-de-negocios-pdvsa-eni/

Never forget, “when there is blood in the streets, buy property”.

LikeLike

Pray tell, how much money does FONDEN have? With links to official sources, bitte

LikeLike

Really? You really don’t get it right? There are no Fonden figures, no one knows the exact numbers. Why do people keep trying to analyse Venezuelas’s economy as if it were a developed economy? Yes, it can be done for comparative purposes, understanding how bad the country is, etc, but it is not helpful for taking decisions going forward. I’m merely telling you what the rules of the game (or lack of rules for that matter) are. Break it down to the basic facts: 1) Venezuela sells between 2mm to 3mm barrels of oil per day. 2) A large percentage of its majority seem to be agnostic to the reality that they can’t save or achieve a decent standard of living. They just don’t care that their currency has been destroyed against all other currencies (99% currency depreciation and devaluation over the last 14 years. 3) A large portion of the population is deeply anesthetised (e.g. People laughing while queuing for three hours waiting for basic products/consumer staples and then laughing when these are THROWN at them) and the Govt. will probably keep its policy of give them the minimum possible so that they keep staying with the big chunk of money . 4) They have numerous measures they can still take to preserve the status quo and people will probably not react, because well, if you don’t really overthrew 3 years ago a Govt. who already had done what it had done, then why do it know? The social profile hasn’t improved, it actually has moved in a direction that favours the Govt. (that means worsened in a developed market mindset). Standards are just so low.

In the meantime, why don’t we focus on the important things that can actually have a material impact not on the price of the bonds in the short term but in the factors that determine the solvency in the long-run? That is the price of oil of course (not that difficult).

Instead of repeating the same idiotic and simplistic economic analyses which are also used by opposition incompetents, we should be increasingly discussing about shale gas/oil and the future of energy consumption. Just saying.

LikeLike

I hope you’re only handling your money and not someone else’s. You have a knack for only loooking at half the story.

This post is about governement spending and BCV reserves falling. Then you come and say that BCV reserves are not important because “[well informed people like you] know the money is not in BCV but in FONDEN and whatever other funds”. Clearly, in order to know this for sure, a balance is needed, otherwise it could have already been spent. But you know it in your heart of hearts, I guess.

Now you say that should focus “in the factors that determine the solvency in the long-run? That is the price of oil of course (not that difficult).” Well, genius, oil prices are only half the equation. We need to look at revenues AND expenses to determine solvency.

Sheesh.

LikeLike

Well, setting aside the fact that Venny Trader is clearly a Gold Star Asshole, his initial “pero” is not really wrong, as today’s post explains. (How exactly knowing there’s some additional mystery figure that may or may not be zero backstopping the announced reserves is supposed to *bolster* your confidence in the government’s creditworthiness is sort of beyond me, but then that’s why I’m not a Wall St. shark, I guess… :)

LikeLike

Well Francisco, considering some of your replies to fellow readers of your blogs, let’s say the you are very close to me in the asshole scale. However, this time, I’d rather be an asshole who is on the correct side of things.

I’ve expressed my opinions on Venezuelan finance matters before. It has always been similar as I think the underlying assumptions of my reasoning haven’t changed that much. As opposed to other readers, I am not a specialist-du-jour and limit my comments to the only fields I know about, finance and investments.

So really, the fact that this Govt. has punctually paid every single coupon and principal linked to its different debt issuances in the last 14 years (despite coups, oil strikes, tech bubbles, financial crises) doesn’t really mean anything to you in terms of creditworthiness? Should I just only pay attention to what Miguel A. Santos,Jose Guerra, et al say then? Or should I just listen to Standard & Poors (in reality called Poor Standards) who rated securitised junk debt AAA pre-financial crisis?

I’d rather not too, they add too much noise. As you well described in one of your posts a few days ago, it is crucial to identify noise when analysing Venezuela both politically and economically. And well, they don’t teach many of the unconventional methods in books.

LikeLike

Really J. Navarro? I really didn’t know solvency was determined by both revenues and expenses, thanks for the heads up.

Clearly, you don’t understand how the Govt. has managed to capitalise on Venezuelan’s poor living standards for so many years. This is populism on steroids. Relatively to what the govt. earns, the expenditures are peanuts and can be cut further. Look at what happens now. Does the vast majority of the population really care if they have to queue 3 hours to buy sugar or other product? Well, it looks like they complain here and there, but in the end, the majority doesn’t even care or can’t at least get organised to change their politicians.

Again, you keep looking at Venezuelan economy like if it where a 2+2=4 and it is not the case. We have more in common with other oil producing countries like Nigeria and Iran than with neighbouring countries like Colombia.

LikeLike

Once again , people are so sure that once an oil production is achieved it just stays there forever that some clarification is in order . As fields age they start reducing production steadily so that to keep production going you have to invest heavily and constantly . If you wait long enough the lost production becomes irrecoverable . the more you wait to make that investment the more difficult and costly recovering production becomes .For years now Pdvsa has been neglectful of doing those investments, its operational infrastructure has become more and more inept and incompetent , the money is spent on govt programs that keep people happy but that dont maintain production , the priority is always winning the next election . thats been going on for years, now Venezuelas light medium crude fields (that bring in the most money) have started declining production sharply , lots of production has been lost and recovering/increasing that production means some pretty heavy investment by people with top knotch technical know how , that means bringing outside help (pdvsa hasnt got the money or the expertise) , companies with big pockets, because foreign companies have been treated so shoddily not every company is willing to come unless they are given iron clad security of getting their money back and ultra high profits. Pdvsa has embarked on a process for signing up these companies to help restore increase production. Additionally more and more of the oil consist of extra heavy crude oil which is very expensive to produce upgrade and market, these latter projects take years and years to develop and again first class international investors are needed having both the money and expertise to carry them through . Venny just takes it for granted that the oil production will remain at 2 to 3 million bls day and that all oil bring in the same income . The fact is that oil prices are not homogeneous throughout the world nor for every kind of crude , extra heavy crudes are much more expensive to produce , require very large initial investments are more difficult to market and bring in lower prices than ordinary crudes, as Venezuela become more a heavy crude oil exporter this is going to have an effect . the other factor is that while in the past venezuela sold much of its crude in the form of refined products which bring in higher prices now the refineries are operating at a much lower level, with higher costs so that less income is generated by them. Oil cannot be treated so simplistically. Even if Pdvsa manages with luck to meet all these challenges and maintain or increase production it will not necessarily be getting the same income as it did in past years , in part because miuch of the newly generated money will go towards paying investors and contractors and financiers for the huge investment they are putting up !!

LikeLike